Google Stock: Deep Recession Value (NASDAQ:GOOG)

Sean Gallup/Getty Photos Information

Google’s mum or dad firm Alphabet (NASDAQ:GOOG) (NASDAQ:GOOGL) is likely to execute a 20-for-1 stock split in July, and I feel traders may possibly want to take into consideration the inventory prior to it splits. The enormous inventory split will make Google stock substantially far more reasonably priced for buyers interested in the business, and the superior selling price of $2,180 has very likely held back need. Right after a 24.6% fall in pricing this year, shares of Google depict strong (recession) benefit and the inventory break up could be a catalyst for an upleg!

The Forthcoming Stock Split Could Be A Catalyst For Google

Google was not the only firm that introduced a stock break up lately. Amazon (AMZN) also executed a 20-for-1 inventory break up, whilst Tesla (TSLA) plans to break up its stock in a 3-for-1 deal. E-Commerce company Shopify (Store) just executed a 10-for-1 stock split, but the stock has, in spite of the likely break up catalyst, less than-performed anticipations.

Companies break up their stocks to make them more economical for traders, normally after a content stock rally has taken position. Google’s stock break up is predicted to be done on July 15, 2022, which is when shares are likely to trade at the split-modified cost. Shares of Google at the moment trade at $2,182, implying that the break up altered selling prices will be around $109 (1/20th of the pre-break up selling price), but the math could surely alter till July 15, 2022. If Google’s shares were being to go by way of however a further drop in pricing pre-split, this lower cost amount would of program be taken care of submit-break up.

Inventory splits only superficially influence the affordability of a inventory, which indicates that valuation ratios are not affected by a inventory split alone. Having said that, stock splits could end result in improved investing and higher rates post-split, as extra traders can obtain a inventory that they may possibly have considered as out of arrive at in advance of the break up.

Google Has Monumental Recession Benefit

Now that the market place is bracing for a economic downturn, traders may perhaps want to think about investing in corporations that are likely to grow their major strains, free funds flows and earnings in spite of escalating economic headwinds. I feel Google signifies enormous price through a recession simply because the research big will continue to grow its company even when the financial state as a entire commences to wrestle. The essential cause for this belief lies in Google’s strong current market place in search and the good business enterprise traits in cloud computing.

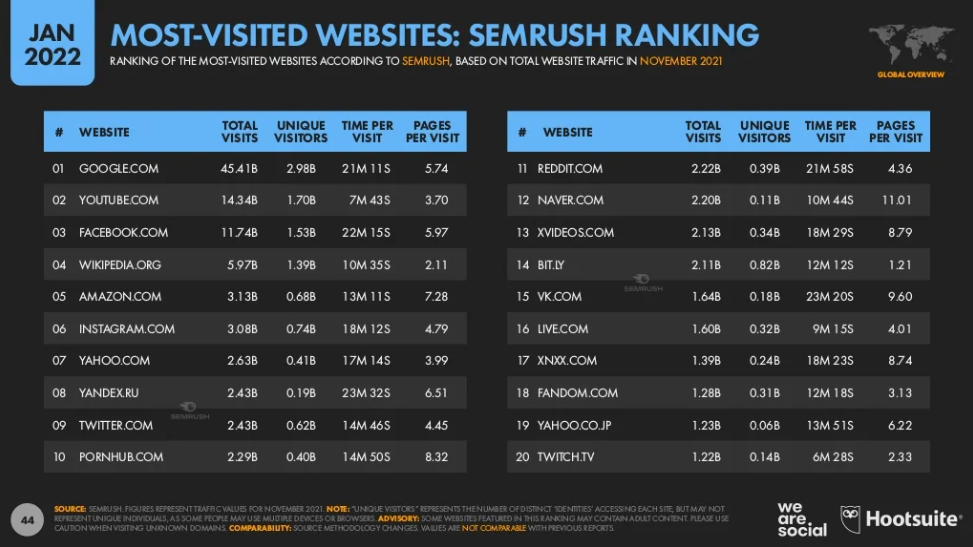

Centered on details from Hootsuite, Google.com and YouTube.com are the two most-frequented websites in the environment (exterior of China) which produces a foundation for sustainable development in marketing revenues. Proudly owning the two most-visited internet websites has massive value for Google and its shareholders: Google created around 58% of its full revenues in Q1’22, a full of $39.62B, solely from its Google Look for-affiliated enterprises.

Hootsuite

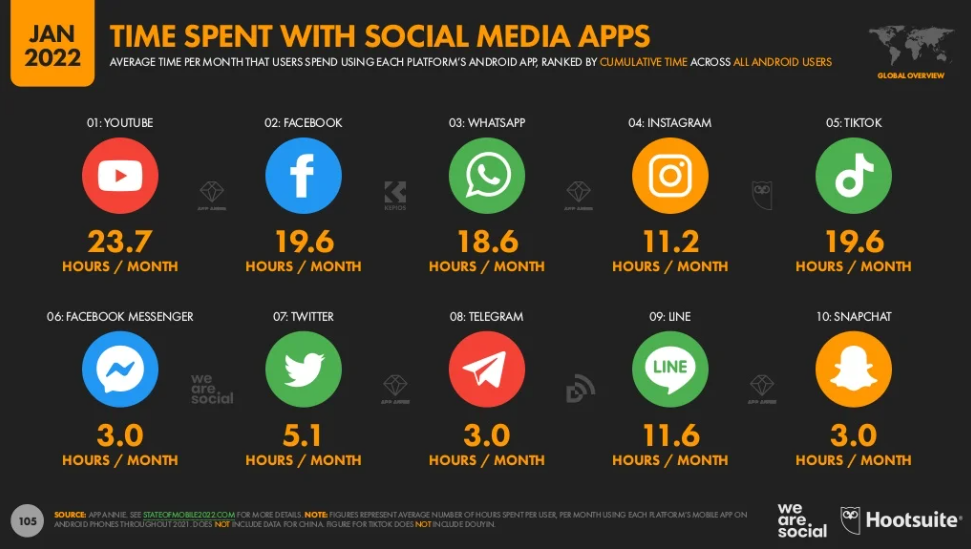

Also centered on the Hootsuite Electronic 2022 Worldwide Overview Report, Google-owned YouTube is, by significantly, the most effective social media platform relating to capturing users’ attention. On average, people spent an regular of 23.7 hrs a month on YouTube, which conveniently conquer out rival social media platforms like Facebook, Instagram and TikTok. Revenues from YouTube ads soared 14% in Google’s very first-quarter, reaching $6.87B and represented a 10% revenue share.

Hootsuite

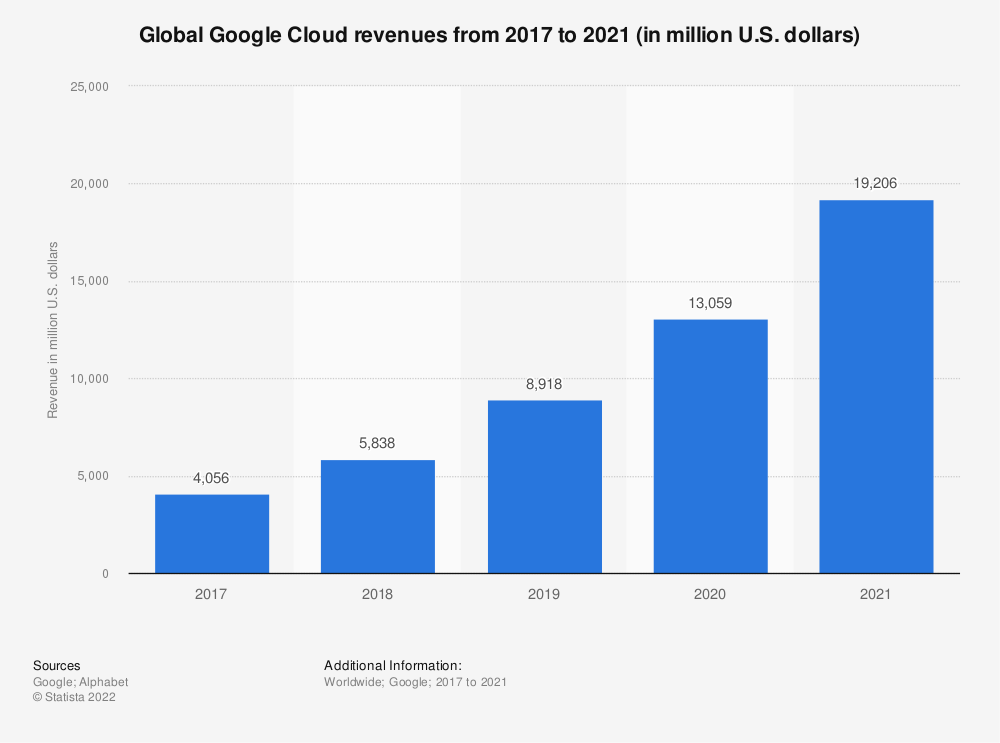

Google Cloud Revenues Are In An Upswing

Google’s cloud organization is gathering momentum, and the company has witnessed a strong boost in revenues in the past 5 several years. Google cloud revenues chiefly incorporate fees for the provision of infrastructure, platform, and other products and services. Google’s cloud revenues greater by a element of 4.7x involving FY 2017 and FY 2021 to $19.21B and in Q1’22, the cloud company was the speediest rising company phase inside Google with a development amount of 44%. The cloud section grew 80% more rapidly than Google’s lookup organization, which grew at a 24% amount yr about year in Q1’22.

Statista

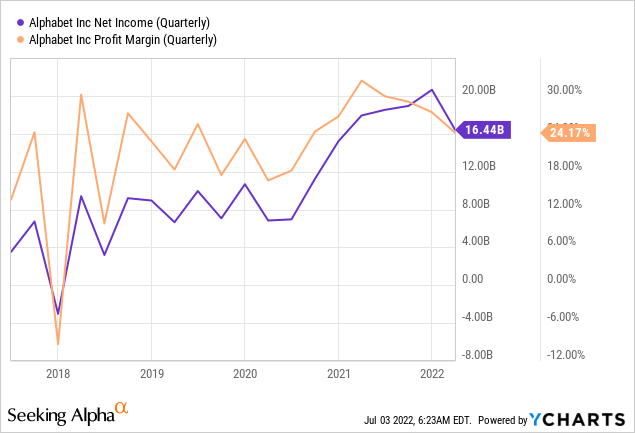

Google’s look for business generates predictable revenues for the company for the duration of a economic downturn, when the cloud small business could produce additional growth. In the course of recessions, predictability of revenues and income circulation has fantastic benefit for traders, and it boundaries stock risks. Google also is an unbelievably rewar

ding organization, mainly due to the fact of its look for organization, and the enterprise now achieves web financial gain margins earlier mentioned 20%.

Google Continues to be Affordable

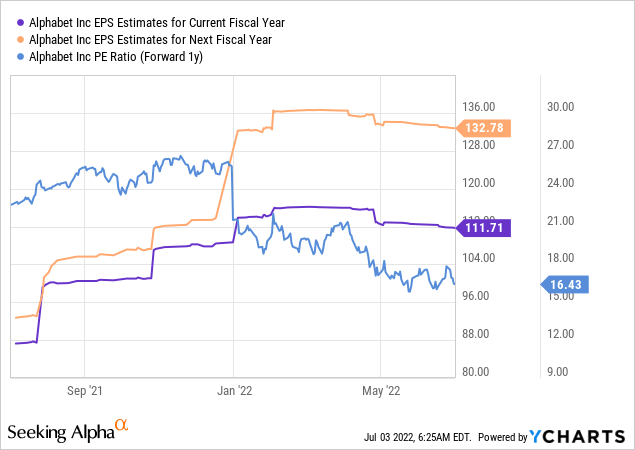

Consensus profits forecasts suggest average annual top rated line development of 13% for Google involving FY 2022 and FY 2027. Based off of subsequent year’s EPS, Google now has a P-E ratio of 16.4x, which I believe that undervalues the firm enormously.

Google’s Funds/Investments Depict Deep Worth And Reduce Threats

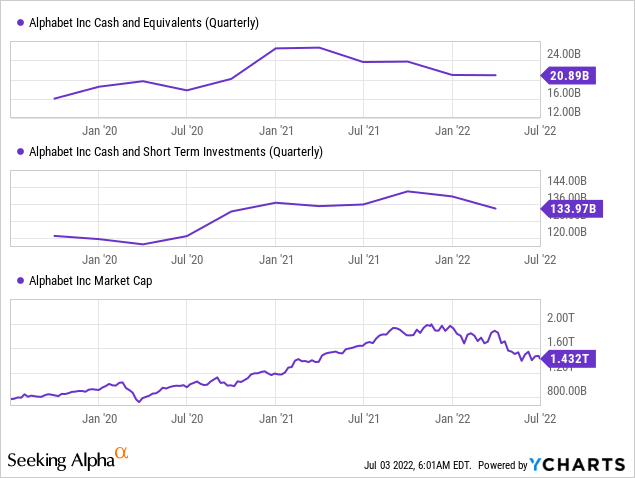

What also lowers inventory hazards for Google is the huge volume of absolutely free funds move the enterprise generates. Secondly, Google is incredibly properly capitalized. The firm’s balance sheet showed $133.97B in complete money and investments at the conclusion of March, which signifies close to 9% of the company’s overall marketplace cap.

Pitfalls With Google Inventory

You will find a quick-phrase hazard that Google underperforms immediately after the stock split is completed in July, and there is certainly no assurance that the research huge is going to do as perfectly as predicted. Slowing leading line development heading ahead is a respectable issue, but with Google possessing the two most-visited internet sites in the English-talking environment, I think the threats are very a great deal managed. What would adjust my mind about Google is if the firm ended up to see a spectacular slowdown in the cloud business and a decrease in totally free hard cash circulation had been to arise.

Ultimate Thoughts

Google is likely to trade a whole lot closer to $100 in two months, which opens up a total new segment of potential customers for the stock that had been priced out of the current market when the stock traded previously mentioned $2,000. I also believe that that Google has massive recession price for traders mainly because of the energy in the cloud business, huge free hard cash movement and a massive pile of income/investments sitting on the firm’s harmony sheet. I think investors may possibly want to look at purchasing Google pre-split and keeping the inventory by a recession.